Finn ut mer om hvordan vi bruker informasjonskapsler (cookies) for å gi deg en bedre brukeropplevelse.

The Co-operative Housing Federation of Norway (NBBL)

The Co-operative Housing Federation of Norway (NBBL) is a national membership association that represents 41 co-operative housing associations—so-called building co-operatives. 14 700 housing co-operatives and condominiums, counting 570 000 housing units, are managed by these member associations. The 41 associations have a total of 1 135 000 members.The housing cooperative movement started to grow in Norway in the 1920s, and in 1929 the first cooperative housing association (building cooperative), OBOS, was established in Oslo. The chosen model was strongly inspired from HSB in Sweden. However, it was not before after the Second World War that the housing cooperative system expanded through numerous local associations.

A national umbrella organisation was founded in 1946 (NBBL – The Co-operative Housing Federation of Norway). The Norwegian housing cooperative model related to NBBL is based on membership and ownership both in:

- Cooperative associations: i.e. the housing developing mother or secondary cooperatives that sell the housing units to:

- The housing cooperatives: i.e. daughter or primary cooperatives that consist of a specific number of dwellings owned jointly by the residents (owner-occupied housing within a cooperative).

This double membership model is regulated through two sets of laws: The Cooperative Housing Association Act and the Housing Cooperatives Act. The two laws go under the joint name of Housing Cooperative Laws. The laws were first established in 1960 and went through major revisions in 2005.

During the first three decades after the Second World War, the authorities very much used the housing coop system as a “tool” as they carried out a “social housing policy” in close partnership with local authorities and the central government. The cooperative model had the benefit of easy access to community-land and finance trough the State Housing Bank. Up to the mid-1980s purchase and sale of coop dwellings were subject to public price-control. This price-control-system had various “gaps” and weaknesses and was abolished by political authorities.

The change in housing policy from the 1980s forced the cooperative housing system to a fundamental reorientation towards the free marked and more competition. While the housing developing activity in the cooperative associations historically was carried out in collaboration with the municipalities, they now must adapt to a fluctuating market – characterized by a high degree of economic risk. This implies that new housing projects initiated by cooperative associations generally are offered at market prices. However, the surplus from projects is put back into the core businesses in the best interest of their members.

The vision of the Norwegian Cooperative Housing Movement is to offer its members the opportunity to acquire a decent home in a sustainable living environment. NBBL believes in the ethical values of honesty, openness, social responsibility and caring for others, thus adhering to the cooperative principles stated in the International Cooperative Alliance (ICA).

Finance and funding

Historically financing of housing coops were almost exclusively financed through The State Housing Bank, whereas today financing is primarily done through private banks. There is no governmental financial assistance to the construction of housing cooperatives, except in cases when projects are aimed towards people with disabilities or other specific population groups.

For the housing coop the collective loan covers up to 75% of the price of a new housing project and its dwellings. The rest is covered by initial capital paid by the members of the coop. The members finance their individual initial capital by a loan from a bank and/or own savings.

Members pay a monthly fee that covers interest and amortisation expenses of the cooperative’s loan, as well as the operating expenses and scheduled future maintenance. The monthly fee is related to the size of the unit the member occupies. Members are responsible for the repairs and maintenance of their own units and the cooperative is responsible for the maintenance of common areas and facilities.

Every member have ownership rights to a certain apartment in the building. This can be sold at market price but is linked to a system of pre-emption right for other owners/residents in the same housing coop and for members in the cooperative housing association (the mother org.).

Size and scale

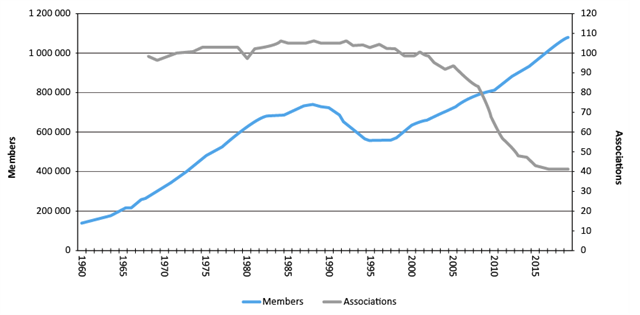

With one exception, all major cooperative housing associations are members of NBBL. The 41 member associations of NBBL are scattered throughout the country but play a major role primarily in the larger cities. During the last twenty years, the number of associations has more than halved due to comprehensive merger-processes. On the other hand, the numbers of individual members have grown substantially: Today the 41 cooperative housing associations have more than 1 million individual members. The largest one (OBOS), that has merged with several other associations in different parts of the country, is in 2020 approaching half a million members. However, most of the 1 million members in the 41 housing associations are not living in a housing coop. They are just members of “the mother” organisation, that gives pre-emption to buying both new and second-hand dwellings (in affiliated housing coops).

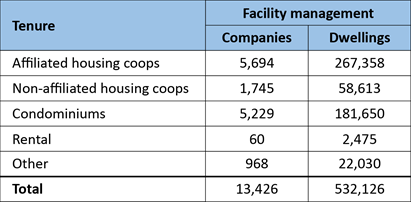

The total number of cooperative dwellings in Norway is approximately 350,000 (13-14% of the total stock of dwellings). Nearly 270,000 of those are established by the NBBLconnected associations distributed in 5,700 so called affiliated housing coops. The cooperative housing associations are major players in the marked of facility management, and the completely dominant ones concerning housing coops:

Purpose and role in society Even though the social role of housing coops was reduced following the reduced public economic support and the liberalisation of the housing market, the housing coop sector still plays a very important role in the Norwegian housing sector:

- As a group, the cooperative housing associations represent a major housing developer in Norway. In the period of 2015-2019 the cooperative housing associations developed approx. 4,000 housing units pr. year, which is 10-15% of the total number being built. A good proportion of these dwellings are in a Norwegian context considered “affordable housing” – even though the housing cost can be rather high compared to average levels in the exciting housing stock.

- NBBL is therefore fighting for better conditions for both the development of new houses, and for ordinary people’s ability to acquire a decent home. For the time being quite a few cooperative housing associations are involved in new projects that aim for an easier way to enter the housing market – especially for young first-time buyers (rent-to-own projects).

- Cooperative housing associations are engaged in quite a few new housing projects in close connection with municipalities, even though the number has diminished over time. This will typically be projects (partly) aimed towards disabled and/or elderly people, but in some cases also the youth.

- The 350,000 cooperative dwellings in Norway represents an important housing supply - especially for small households with low and medium income. The yearly turn-overrate for coop dwellings is close to 10%.

- Especially concerning apartment buildings, the cooperative housing associations are the dominant player in the marked of facility management. To provide good maintenance services to housing coops and condominiums is a major task and a social mission for the cooperative housing associations. We are facing huge challenges connected to making the existing housing stock more sustainable – socially, economically and environmentally – and the cooperative housing sector in Norway wants to play an important role in this transaction.